If you run an SME in the Middle East, you already know: uncertainty is not theoretical. It is operational.

From geopolitical escalations to currency fluctuations, trade route disruptions to shifting regulatory landscapes, the region has seen wave after wave of volatility. For small and medium enterprises, each wave carries the same two risks: cash flow shock and decision paralysis.

The first drains your runway. The second freezes your leadership. Together, they can turn a temporary disruption into a permanent setback.

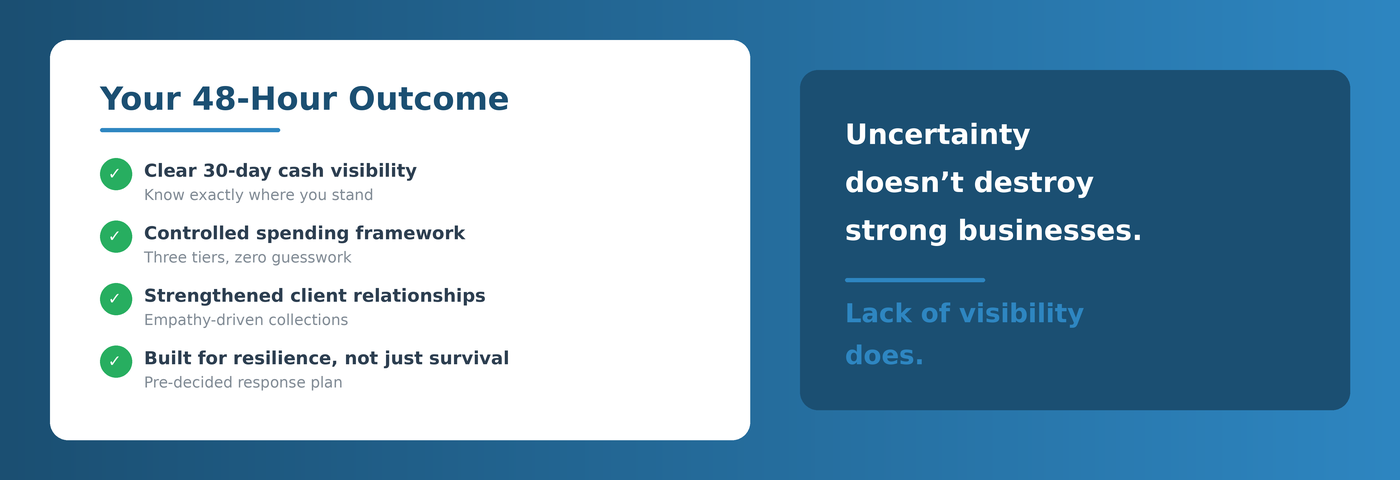

But here is the reality most business owners overlook: you do not need weeks to regain control. You need 48 hours.

Based on our work with multiple SMEs across the UAE and Bahrain, we have distilled the most critical early moves into three actions. These are not theoretical frameworks. They are the exact steps that separate businesses that survive disruption from those that get consumed by it.

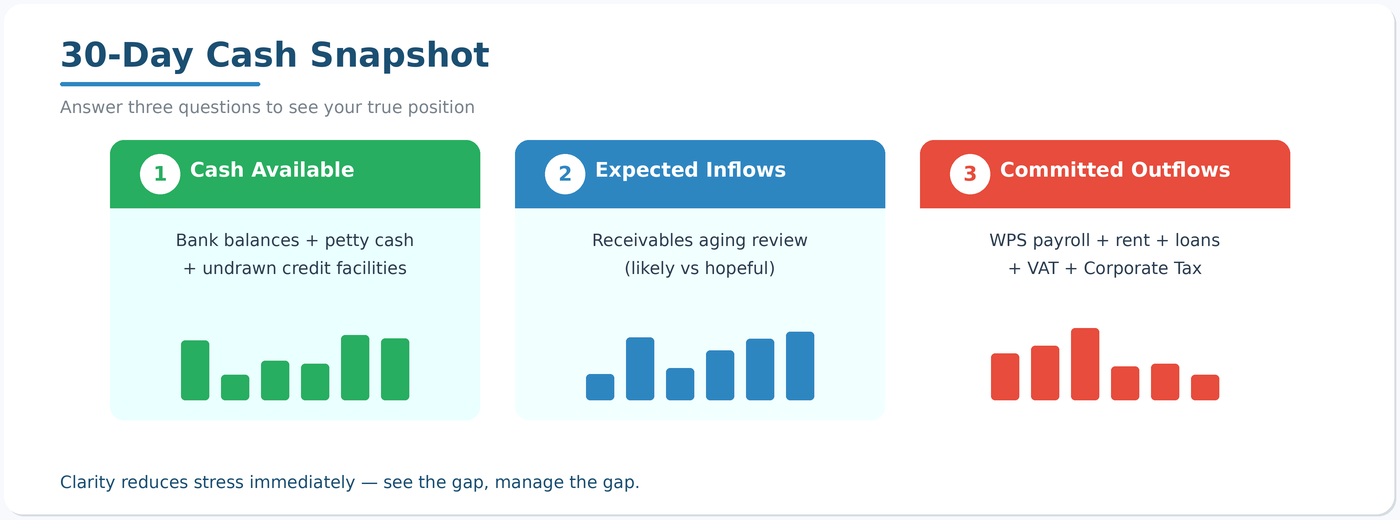

Action 1: Map Your True Cash Position in 24 Hours

The problem: Most SME owners think they know their cash position. They check their bank balance and feel reassured. But a bank balance is not a cash position. It tells you what is in the account right now. It says nothing about what is coming in, what is committed to go out, and when the two will collide.

The action: Within the first 24 hours of any disruption, build a simple 30-day cash snapshot. This is not a full financial model. It is a one-page view that answers three questions:

- How much cash is actually available right now? This means bank balances across all accounts, petty cash, and any undrawn credit facilities. Not projected revenue. Not pending invoices. Actual, accessible cash.

- What money is realistically expected in the next 30 days? Review your receivables aging report. Separate the likely collections from the hopeful ones. If a client has been late three times in a row, do not count that invoice as a sure thing.

- What absolutely must go out in the next 30 days? Payroll commitments under WPS. Rent. Loan repayments. VAT obligations. Corporate Tax instalments. Critical supplier payments that keep your operations running.

Why it matters: In our experience, SME founders who complete this exercise report an immediate stress reduction. Not because the numbers are always good, but because ambiguity is more damaging than bad news. When you can see the gap, you can manage the gap. When you are guessing, you are paralysed.

This is exactly why Daira built the OneFinance™ Dashboard: to give SME owners this visibility in real time, not just during crisis moments, but as a permanent operating advantage.

Action 2: Prioritise Costs Intelligently, Not Emotionally

The problem: The moment uncertainty hits, the instinct is to cut. Cut marketing. Freeze hiring. Cancel subscriptions. Renegotiate everything. And while the intention is survival, the execution often damages the business more than the crisis itself.

We have seen SMEs slash their sales team budget during a downturn, only to realise three months later that they had no pipeline to recover with. We have seen businesses cancel their accounting software to save AED 500 a month, then miss a Corporate Tax deadline that costs them ten times that in penalties.

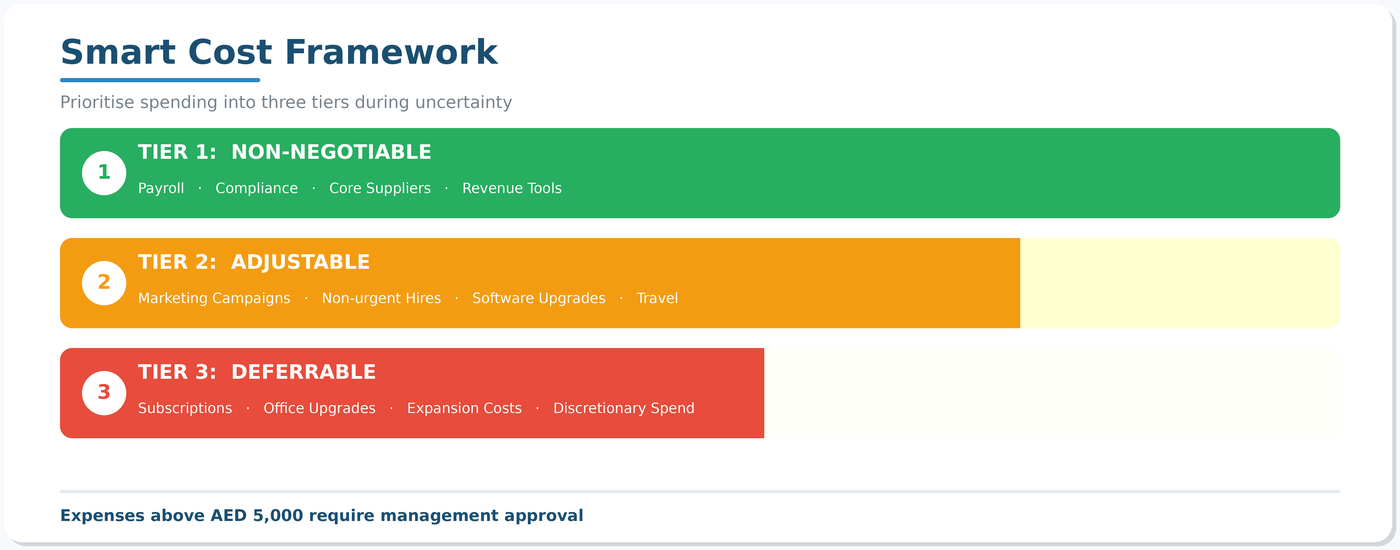

The action: Instead of making blanket cuts, create a simple three-tier cost framework within 48 hours:

💡 Founder Tip

Tier 1 -- Non-Negotiable. These are costs that directly protect revenue or compliance. Payroll for revenue-generating staff. Compliance and bookkeeping services. Core supplier relationships. Cutting these does not save money; it destroys your ability to earn.

Tier 2 -- Adjustable. These are investments that matter but can be dialled back temporarily. Marketing campaigns can be narrowed to higher-ROI channels. Non-urgent hires can be paused. Software upgrades can wait 60 days. Travel can shift to virtual.

Tier 3 -- Deferrable. These are discretionary costs with no immediate impact on revenue or compliance. Nice-to-have subscriptions. Office upgrades. Expansion-related expenses. These get paused until visibility improves.

Then implement one simple rule: no new expenditure above AED 5,000 gets approved without founder review for the next 30 days.

Why it matters: This is not about being fearful. It is about disciplined capital allocation. The businesses that emerge strongest from volatile periods are never the ones that cut the most. They are the ones who cut the right things and protect their earning capacity.

Action 3: Strengthen Client Relationships and Manage Collections with Empathy

The problem: In volatile times, the instinct is to chase every outstanding dirham aggressively. But here is what many SME owners forget: your clients are navigating the same uncertainty you are. Their budgets are tightening. Their approvals are slowing. Their finance teams are conserving cash, just like yours.

If your first move during a crisis is to pressure clients for faster payment, you risk something far more expensive than a delayed invoice: you risk losing the relationship entirely. In a market where trust is built over years and lost in a single interaction, aggressive collections during a shared crisis sends the wrong signal.

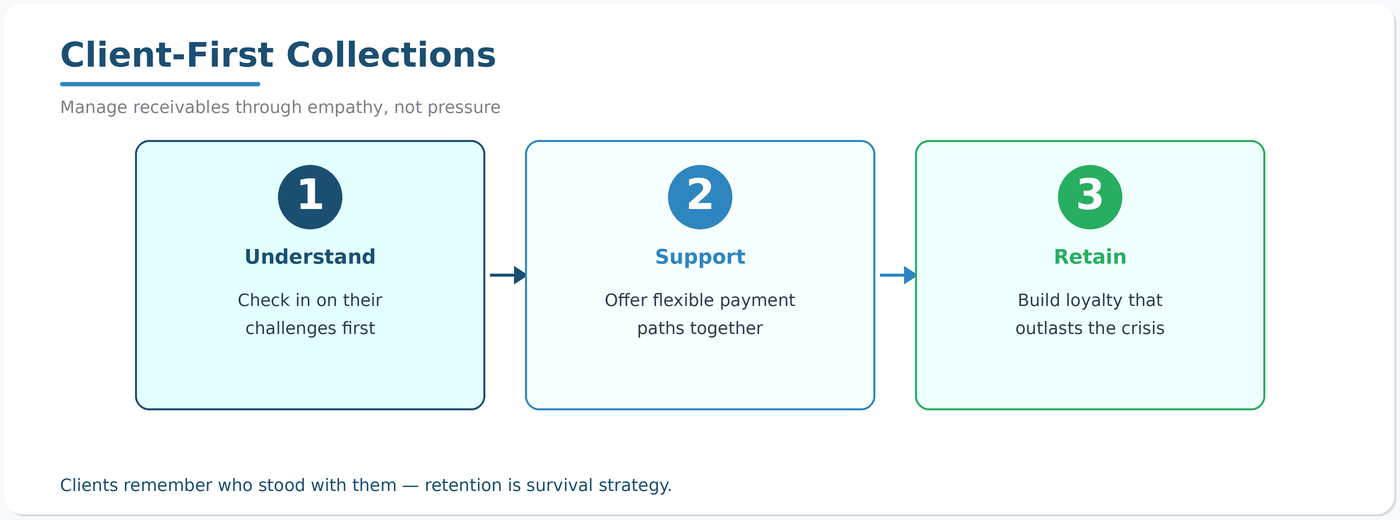

The action: Within 48 hours, identify your top 10 outstanding receivables by value. But instead of launching a collections sprint, launch a client check-in. The goal is twofold: understand their situation and find a path that works for both sides.

Pick up the phone. Not to demand payment, but to have a real conversation: "We know things are uncertain right now, and we want to make sure we're supporting you through it. Can we talk about where things stand and how we can work together on timing?"

This approach achieves several things at once:

It preserves the relationship. Clients remember who stood with them during difficult times. When conditions improve, and they always do, the businesses that showed empathy are the ones that get renewed, expanded, and referred.

It surfaces real information. A genuine conversation reveals whether a client is temporarily delayed or genuinely struggling. That distinction changes how you plan. A client who says, "We can pay 60% now and the rest in 45 days" is very different from one who goes silent.

It opens the door to creative solutions. Perhaps you offer a short-term payment plan. Perhaps you can restructure the engagement to reduce their monthly commitment while maintaining the relationship. Perhaps you provide additional advisory support that helps them through their own cash crunch, deepening the partnership.

Why it matters: In our work across the UAE and Bahrain, the SMEs that retain the highest percentage of clients through downturns are never the most aggressive collectors. They are the ones that treat collections as a relationship management exercise, not a recovery operation. The maths is simple: acquiring a new client costs five to seven times more than retaining an existing one. During uncertainty, retention is not just good service. It is a survival strategy.

Even with this empathetic approach, you will often find that 20 to 30 percent of outstanding receivables accelerate naturally. Clients appreciate the outreach. They prioritise partners who communicate. And a business with AED 500,000 in receivables that recovers AED 100,000 to 150,000 faster, simply by having honest conversations, has meaningfully extended its runway without damaging a single relationship.

The Bigger Picture: Why This Matters Beyond the Crisis

These three actions are not just crisis tactics. They are the foundation of how well-managed businesses operate at all times. The difference is that in stable periods, you can afford to be approximate. In volatile periods, approximation is a luxury that turns into a liability.

There is also a leadership dimension that most articles on financial management overlook. Your clients are watching. Your team is watching. When you demonstrate discipline and structure in how you manage your own finances, it builds trust. Clients do not just buy services during uncertain times. They buy stability, predictability, and confidence.

The SMEs that come out of disruption stronger are not the most aggressive. They are the most disciplined. And discipline starts with visibility.

How Daira Can Help

At Daira, we work with SMEs across the UAE and Bahrain to build exactly this kind of financial clarity. Through our OneFinance™ Dashboard, you get real-time visibility over cash flow, receivables, payables, and compliance obligations, all in one place. Our Business HealthCheck™ gives you a structured diagnostic of your financial resilience, so you know where you stand before the next disruption arrives.

If you want to run through these three actions with real numbers, not hypotheticals, we offer a complimentary 30-minute stability assessment for SME founders.

Reach out to us at contact@daira.me or visit www.daira.me

Clarity beats chaos. Every time.

Topics